Why Do Banks Suddenly Offer High Interest Rates?

A timetable is forming

Come on, it’s only (your) money.

Banks want your money

Certificates of Deposits (CDs), savings accounts, and Money Market accounts are now offering higher interest rates than most of the time before. According to Forbes, as of October 19, 2023, the

Highest CD Rates

Banks and credit unions offering the best CDs pay higher APYs or dividend rates relative to the national average rates. Of the numerous nationwide institutions we monitor, here are the top CD rates by term.

3 months: TotalDirectBank CD at 5.66% APY

6 months: CommunityWide Federal Credit Union CW Certificate Account at 5.50% APY

12 months (1 year): Bread Savings at 5.60% APY

24 months (2 years): PedFed Credit Union Money Market Certificate at 4.60% APY and First National Bank of America Certificate of Deposit at 4.80% APY

36 months (3 years): First National Bank of America Certificate of Deposit at 4.85% APY

48 months (4 years): First National Bank of America Certificate of Deposit at 4.80% APY

60 months (5 years): First National Bank of America Certificate of Deposit at 4.75% APY

Rates are based on a $25,000 minimum deposit and are accurate as of October 16, 2023.

https://www.forbes.com/advisor/banking/cds/best-cd-rates/

If you want to see differences between CDs, Savings accounts, and Money Market accounts, check out this site (you will be allowed to enter a ZIP code, select an amount of under $1,000/$1-5k/above $5k, and select the type of account you would like to investigate):

https://fiona.com/partner/forbes-cd/savings

Stock-market investments have been dead in the US for decades. Only insiders were able to rip off the newbie and the perpetual optimist. This time, a long-unprecedented opportunity to make money out of interests is opening up, which makes putting money in the bank, all of a sudden, attractive. You can say interest rates are raised in order to keep the economy going, but these days are different from the good old ones, when the logic actually worked. One thing is sure: the bankers want your money in their possession. After you give it to them, they will spend it at their own discretion until your money will not be worth a penny even in their hands. You’ll own nothing and they’ll be happy. Happy, but how? I’ll get back to that later.

The good news

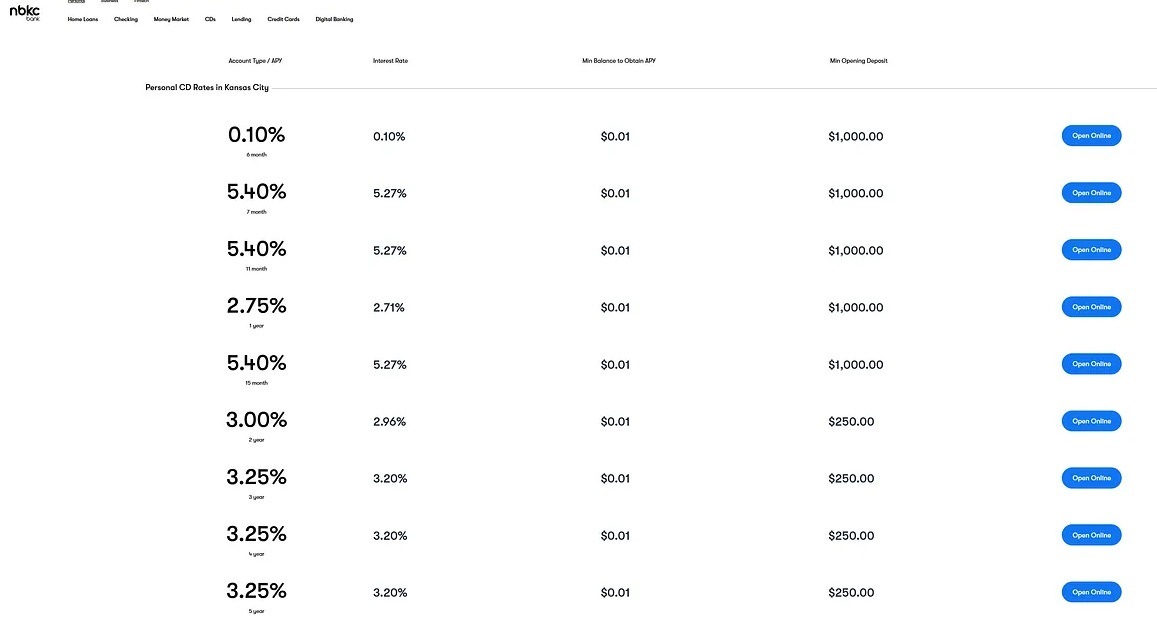

Yet there is some good news, too. To my surprise, an internet bank from Kansas, NBKC, is offering something more instructive for prospective CD owners than the quotes by Forbes:

https://www.nbkc.com/personal/certificate-of-deposits

Why is this good news? I’ll get back to that later, too.

From bank deposits to the CBDC

While all these quotes are for the current USD, you might want to consider that the CBDC already exists in several countries, and its implementation in private life is only a question of time:

As people are not exactly ecstatic about the idea that the amount and their access to their “money” will be determined and limited by the “authorities,” who have copiously demonstrated in the last 100 years or more that they couldn’t care less about the “deplorables.” How is the CBDC going to be forced on the people?

Now, that’s a no-brainer. Just like some companies have been bankrupted by their CEOs or their major stockholders on purpose in the last few decades1, inflationary processes have also been created and elevated intentionally in history before. The controlled demolition of the dollar is in progress2, and once people need a wheelbarrelful of banknotes to buy a bar of soap, they will beg for the introduction of a new currency, and the only offer they will receive will be the CBDC. The ensuing turbulent times will provide excellent cover for the globalist to initiate further events that will also lead to full civilizational collapse, as I described it already on April 26, 2023:

https://rayhorvaththesource.substack.com/p/this-is-how-it-will-go-down

The writing on the wall: a timetable for the financial collapse

High interest rates attract depositors to put their money in the bank. Most people don’t know that they are giving the bank an unsecured loan, insured by the federal FDIC, while the Federal Government itself is rapidly approaching insolvency. Despite the signs of the times, chances are, people will keep their money in the bank.

So, what about the fabulous interest rates on CDs at NBKC? Why would a 6-month CD come with an interest rate of 0.10% and the seven-month with 5.40%? As the sudden leap is inexplicable, to me, it looks like a cautionary indicator of what’s coming. The writing is on the wall, but what does it mean?

The optimistic guess is that perhaps because someone in the “know” is well-meaning again and wants the public to be informed about the upcoming financial collapse that, according to conservative estimates, is inevitable in 6-24 months, so you must prepare for something that will be a lot worse than the Great Depression for several reasons.

Realistically, if popular reaction to the “optimistic” assessment is calculated, people will start picking up cash at their banks. Now, only 1-2 percent of the money in circulation is cash; the rest exists only in electronic form as debts and transactions. Cash transactions will have to be frozen, and the value of your money will become questionable.

It’s logical to assume that the USD is about to be destroyed, so high interest rates will mean nothing after the currency loses its value. There will be many causes for the collapse, but people wanting to save their money by picking up cash will accelerate the process. After the defunct banks are liquidated, the FDIC will be “able” to return 50 cents after each 100 dollars it is “insuring.” As an alternative, people are likely to receive a “generous” offer from the Federal Reserve: they can keep their lost savings, but only in the form of FedNow3.

One way or another, Vanguard, Blackrock, and State Street manage to manipulate an intertwined system of hundreds, if not thousands of companies that produce, manufacture, and distribute essential goods, while their owners also control the banking system. Besides playing hide-and-seek, I’m sure that they often sacrificed some of their assets in order to maximize their profits in their other investments.

The dollar losing its reserve status will likely blamed on the BRICS initiatives (dedollarization and the introduction of their international CBDC for trade), and the international CBDC they are introducing at first will be turned global and will require national CBDCs in order to retain “convertible.”

https://www.federalreserve.gov/paymentsystems/fednow_about.htm

The details will be pretty much the same as in China:

https://rayhorvaththesource.substack.com/p/who-is-the-creditor-for-your-antisocial

Could be a bail-in is in the works??

I keep just enough in my checking account to cover recurring bills and keep it open. As soon as my SS is deposited, I withdraw it.